Where markets and technology meet

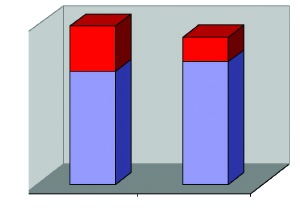

Fig. 1:While innovative products generally have a higher capital costs than traditional approaches, reduced labour costs can bring significant benefits. This example illustrates the installed costs of pipework using a channel system. Material costs are 8.4% higher, but labour costs are 46% lower. The overall effect is a 7% reduction in installed cost.

Progressive companies base their success on a sustained programme of new-product development. Anne King examines the issues in the building-services sector.In competitive markets, new product development is essential if a manufacturer is to stay in business — and even more so to thrive and grow.

Targets Global companies, like Du Pont or 3M have specific targets for new-product development and set an example for all of us. In 3M, 40% of sales must come from products launched in the last four years. Is there any reason why building-services manufacturers should not be as innovative and successful as this? Three reasons are regularly quoted. Reason 1: Clients will not take risks. Quite correctly, clients will not take risks that they do not understand. However, many clients can see the upside of innovation, for example in reduced in installation time or in lower running costs, and seek innovative approaches from their suppliers. In its Prime Contracting Contracts, the Ministry of Defence is looking specifically for contractors who will ‘meet the service delivery specification efficiently, economically, innovatively and on time’. Reason 2: ‘Consultants will not put it in their specification’. Consultants are certainly right to be wary of specifying items where performance is uncertain or where they do not have good information on how to fit the new product into conventional systems. Rod Hickmott of Uponor Housing Solutions recognised the need for a definitive designers’ guide to underfloor heating and a set of inspection standards to encourage wider uptake of the industry’s products. As a consequence, the underfloor heating industry asked BSRIA to compile such a guide. Reason 3: ‘Contractors will not use it because it is more expensive’. If this is really true, it may well be justified. Although contractors should be able to charge a higher margin on a more expensive product, any contractor bidding for a job will tell you that life is not so simple. Using a new product will often cut the overall cost of installation but the materials cost is higher. Fig. 1 shows the relative costs of a traditional channel support system and a new modular system developed by Hilti, as described in BSRIA’s M&E Innovative Datasheet 5.2. Overall, a 7% cost reduction was achieved. Although material costs were a little higher, labour times were nearly halved. Contractors must look beyond the material costs alone. Clients, consultants and contractors are not just being awkward. They are customers of the manufacturing industry, and their views must be taken into account. It comes down to really understanding the market and developing products that meet the market need. Get product technologists and marketing staff working together. New-product development must be accompanied by rigorous market research.

Horizon The market research needs to scan the broad horizon to find the future market drivers, with more detailed research out to examine the opportunities in detail. What might that horizon scanning reveal? New-product developments that succeed are those that have strong drivers behind them. Regulation is the most obvious; look at the developments of compressors and refrigerants. The new Building Regulations Part L consultation document and the report of the Sustainability Task Group should be studied by all manufacturers. Another important driver is change in relative prices; increasing oil prices is an obvious topical example. A third is resource availability; one of the major drivers is the difficulty of recruiting skilled site workers. The very well known PESTEL methodology (which examines political, economic, social, technological, environmental and legal drivers) is a framework for such scanning. The panel below has been generated from a number of different PESTEL exercises that BSRIA has recently carried out with companies. It also includes some outputs of the Think 2010 event organised by the services sector in March 2003 (www.bsria.co.uk/think2010). A PESTEL analysis will vary depending on the context, and this one can only give some very general pointers. More detailed market research — not just of customers but also others in the supply chain — should generate information for a go/no-go decision. It will also help in the setting of prices, designing product ranges, working out the best channels to market and developing a good promotional plan. Other contacts in the industry and in research and academic organisations should be used to help product design. In the HVAC sector, a useful source of contacts is the HEVACR Technical Exchange (web address below). Even when market research indicates a product is the right one in the right place at the right time, there will still be objections to handle. A client’s objections need a good business case. For a completely new product, clients cannot be sent to a reference site, which is what they would like most. However, a product can be independently tested to prove its performance and its durability. If there is no prevailing test standard, a test laboratory will develop one. To handle a designer’s objections, the job should be made easy. Specification clauses should be ready, recognised industry guidance written, and details publish them the Internet. Finally, contractors will need independent information on installation times and reliability, so that they can factor this into their estimates and sell the concept to the client.

Anne King is Marketing director at BSRIA, Old Bracknell Lane West, Bracknell, Berks RG12 7AH. BSRIA’s consultancy services include technical and market support for new-product development. A PESTEL analysis is a valuable approach to new-product development. Here are some key pointers for the building-services sector Political Ethical pressure to drive a fairer distribution of the world’s resources. Increased emphasis on security: • Terrorist threat • Fear of crime Increasing protectionism and fear of decline of the World Trade Organisation. Regulations to reduce hours worked = lower take home pay = growing skills shortage. Government (as client) demands for industry to change — based on sustainability, whole-life costing and better value for money. Compulsory use of competency certificates

Economic Migration of jobs and people: n People want to come to the developed world n Pressure to move construction jobs to the developing world — more prefabrication Oil price rise leading to world slowdown. Increasing awareness of operating costs as the important factor rather than capital costs. Low margins driving skills shortage, reduced possibility for R&D, reduced company numbers in the market. Vertical integration of companies. Corporate social responsibility is real driver to improving shareholder value.

Sociological Tension between corporate objectives and work-life balance. People are the key consideration for business success, but: • Increasing sickness • Increasing self-interest • Demographics/age profile Regulations introduced to ‘force’ all types of diversity in the workplace. Employee isolation and interaction in new working practices — leading to hub and satellite rather than home-working — leading to new forms of buildings. Increased use of computers leading to lower levels of interpersonal skills in young people. Communication problems from international diversification. Deskilling of jobs leads to lower employee motivation. Skills gap or shortage. Multi-disciplinary working on site

Technological More harmonisation of standards across Europe – through European building services codes. High level of ‘e’ activity, including virtual prototype before start of building, e-tendering and e-procurement. The self-maintaining building — using technology now available for cars. Increasing off-site fabrication and pre-packaged system design – potential for deskilling and/or reduction in customer choice. On-site generation — micro CHP and district wide schemes. Widespread use of wireless in preference to cable solutions.

Environmental WEEE Directive (Waste Electrical & Electronic Equipment Directive) leading to: • Technological changes • New structures — e.g. lease, not buy • Higher cost • Retain more old technology Shortage of electrical generating capacity as nuclear phased out and renewables take its place too slowly. Climate change: • Double pressure on carbon (higher temperatures means more air conditioning needed) • Flood protection leading to real emphasis on reducing waste water quantities • Huge opportunity to attract younger generation • UK programme challenges current ‘comfortable’ position Phasing out of HFCs by 2010 — pressure on R&D for replacements — price rises. Water quality and availability become as important as energy.

Legal Increasing legislative burden, e.g.: • Health and safety • Data protection • Intellectual property rights • Working hours restrictions • Design liability rests with contractors All mean higher insurance and construction costs. Building Regulations Part L will impose new requirements giving business opportunity, e.g. in facilities management, because of extension to existing buildings. Contracts continue to act as barriers in general and in collaborative working in particular.

Related links:

Related articles: